Why Switching Mutual Funds Too Often Can Cost You More

Once you have set up a Systematic Investment Plan (SIP) and made your first investment, the hard part is largely behind you, or so it seems. In practice, a different kind of challenge often emerges shortly after: the temptation to keep adjusting.

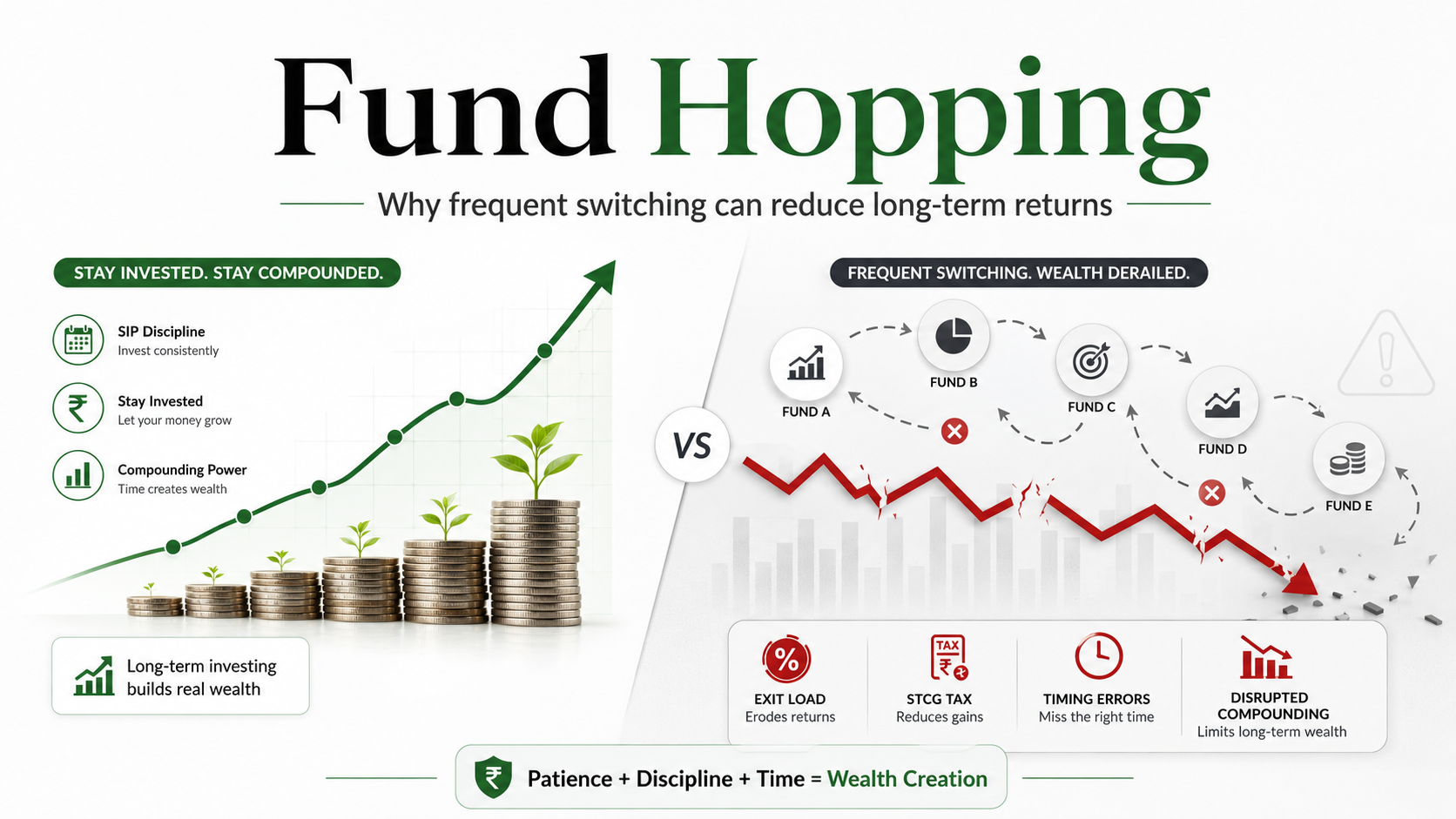

This pattern is known as fund hopping, the habit of selling out of funds that appear to be underperforming and moving into those at the top of the charts. It feels like active portfolio management. In reality, it is one of the most reliable ways to reduce your long-term returns.

An experienced Financial Guide will recognize this pattern immediately. It is not a sign of poor intelligence; it is a very human response to uncertainty. But left unchecked, it can quietly erode years of careful saving.

How the Fund-Hopping Trap Works

The cycle tends to follow a consistent pattern, and it is easy to see how a rational, well-intentioned investor can fall into it:

- The Surge: A particular sector or fund delivers impressive short-term returns, drawing widespread attention.

- The Switch: Feeling they are missing out, the investor sells their existing holdings and buys into the trending fund, often near its recent peak.

- The Correction: The momentum fades. The newly purchased fund falls in value. The investor is now holding a loss, and the original fund they exited has quietly recovered.

This cycle can repeat multiple times, with each switch introducing costs and compounding disruption. The investor feels active and engaged, but their portfolio is quietly falling behind.

Three Hidden Costs of Switching Too Often

1. Compounding Requires Continuity

Compounding works over time, and it works best when it is uninterrupted. Every time you exit a fund and reinvest elsewhere, the growth clock resets. The units you sold are no longer in your portfolio to recover and grow. Over a decade or two, the difference between staying invested and switching regularly becomes substantial, not because of the individual switches, but because of the accumulated effect of all the restarts.

2. Each Switch Carries a Financial Cost

The chart below illustrates the long-term impact of switching costs on a ₹30 lakh lump-sum investment over 20 years.

The figures used above are purely illustrative and are not indicative of future returns.

Every manual switch at the retail investor level can trigger exit loads, typically around 1% if redeemed within one year, along with short-term capital gains tax on any profits. These costs may look small in isolation, but over time, they reduce the investment base on which future returns are calculated.

A fund manager operating within a single diversified fund can rebalance the underlying portfolio without creating these direct costs for the investor. But when an investor tries to replicate this process manually by frequently switching funds, the investor bears the full cost of exit load, taxation, and timing mistakes.

For example, on a ₹30 lakh lump-sum investment, the gap between a disciplined investor and a frequent switcher can exceed ₹1 crore over 20 years. This difference is not necessarily created by better fund selection, but by avoiding the drag of repeated switching costs and timing errors.

3. Constant Monitoring Leads to Worse Decisions

A fund-hopping strategy demands continuous attention: tracking performance across multiple funds, reading market commentary, and making allocation decisions month after month. This level of involvement rarely improves outcomes, it usually makes them worse. The more frequently an investor reviews their portfolio and feels compelled to act, the higher the likelihood of a decision driven by short-term anxiety rather than long-term strategy.

A More Effective Approach

Use Structures Designed for Diversification

Rather than manually moving between funds to capture different market opportunities, consider structures that do this work internally. Diversified funds combine multiple asset classes within a single investment structure. The fund management team rebalances the portfolio in response to market conditions, without triggering tax events for the investor and without requiring any ongoing decisions on your part.

Automate and Step Back

A recurring monthly SIP into a well-chosen, diversified fund removes the need for regular decision-making. When markets dip, your SIP automatically purchases more units at lower prices. When markets rise, your existing holdings benefit. The strategy works through consistency, not through active management, and consistency is far easier to maintain when it is automated.

Measure Performance Over the Right Timeframe

A fund that underperforms for six months is not necessarily a poor fund. Most well-managed diversified funds go through periods of relative underperformance, particularly when a specific sector is driving short-term returns. Evaluating a fund over three to five years, rather than quarter by quarter, gives a far more meaningful picture of whether it is doing its job.

How a Financial Guide Helps You Stay the Course

The urge to switch funds is strongest precisely when staying put feels most uncomfortable, during a market downturn, when a trending fund is generating headlines, or when a colleague mentions a scheme that appears to be outperforming yours. These are the moments when having a Financial Guide makes the greatest difference.

A Financial Guide helps you manage fund hopping by:

- Selecting an initial portfolio structure suited to your goals and risk tolerance, so there is less reason to change it

- Providing context when short-term underperformance feels alarming, helping you distinguish between a fund that needs reviewing and one that simply needs time

- Acting as a check on impulsive decisions, ensuring any change to your portfolio is driven by a change in your circumstances, not a change in the market

- Reviewing your portfolio periodically on a structured basis, so you are not left feeling the need to monitor it constantly yourself

The value of this guidance is not just financial. It frees you from the mental overhead of constant portfolio management, allowing you to focus on your career, your family, and your life, while your investments continue growing in the background.

The Simplest Investing Edge

Long-term wealth is rarely built by the investor who moves fastest. It is built by the investor who stays the longest. Consistency, patience, and the discipline to resist unnecessary switching are among the most powerful tools available, and they cost nothing to use.

If your current approach involves frequent fund changes, or if you find yourself regularly tempted to chase recent performance, it may be worth stepping back and reviewing the structure of your portfolio with fresh eyes.

A Financial Guide can help you build a road map that is simple enough to stay with and robust enough to grow through whatever the market brings.

DISCLAIMER: Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.